Shifting Davis-Bacon Dollars into a Qualified Plan

All businesses experience competition; and to stay ahead, owners continue to look for ways to keep expenses down and put more dollars on the bottom line. In the construction industry, when a company works on state, local, or federal government projects, the employees on those projects can be subject to the Davis-Bacon Act (or similar laws at the state and local level), which requires that the company pay non-union employees the “prevailing” wage and benefits.

Prevailing wage compensation has two parts:

Prevailing Hourly Wage: a minimum basic hourly rate paid at least weekly;

Prevailing Wage Fringe Benefit: paid in the form of either contributions to a fringe benefit plan or paid as cash.

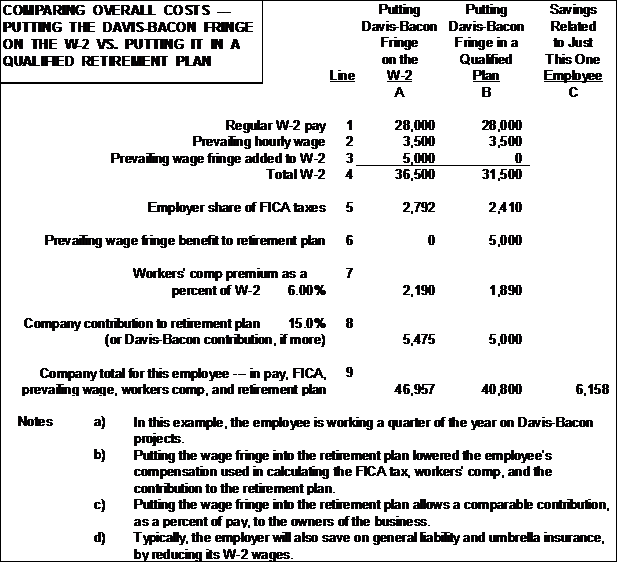

Each year, we see more and more employers choosing to shift the fringe benefit part from the paycheck into a qualified plan, e.g., a profit sharing or 401(k) plan.

The advantages to the employer are savings that could be tens, or even hundreds, of thousands of dollars, due to:

- Elimination of the employer’s part of the FICA and Medicare taxes on dollars put into a qualified plan (totaling 7.65% of payroll).

- Reduction of payroll-related worker’s comp premiums, typically 4% to 7% of payroll.

- Reduction in general liability payroll-related premiums and umbrella insurance premiums, sometimes around 1% of payroll.

An added benefit is that there are also significant advantages to the employees, and this makes it easier for the employer to shift the dollars into a qualified plan:

- Total elimination of the employee’s FICA tax (7.65%) and occupational tax (typically around 1%) on these dollars. We say total elimination, because when these dollars are later taken out of the qualified plan, the FICA tax (and in most cases local occupational taxes) still will not apply.

- Deferral of federal taxes on these dollars:

1) For some individuals, the marginal tax rate in retirement may be lower than the present marginal tax rate.

2) For two-income household’s, if enough of one earner’s wages are shifted to the qualified plan, it may actually reduce the current marginal tax rate on their combined earned income.

- Deferral of state income taxes on these dollars:

1) If retiring in a state with no income tax, then this tax is totally eliminated.

2) For some states, certain types of retirement income are exempt from the retiree’s income tax. For example, in Kentucky, a retiree’s first $41,100 of income, from retirement plans and IRAs, is exempt from state income tax.

- It is not uncommon for every $1.00 reduction in take-home pay to result in over $1.40 going into the plan. In other words, it appears to the employee that the savings in taxes are similar to a match exceeding 40%, even when the employer does not put a match into the plan.

PLAN DESIGN CONSIDERATIONS

- Davis-Bacon dollars can be applied toward minimum requirements for some coverage and nondiscrimination tests required in the plan.

- The ability to make healthier contributions on behalf of management because higher contributions are being made to the plan for the hourly workers.

- Davis-Bacon dollars must be immediately 100% vested.

- The Employer can offset the company’s profit sharing contribution for each participant by the amount of the Davis-Bacon contribution deposited for each participant.